Incident depression and credit scores in U.S. adults, 2023-2025

Abstract

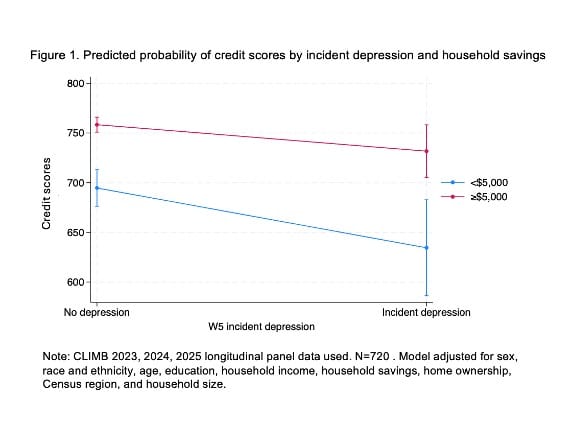

Little to no work has explored the relation between onset of depression and changes in consumer credit scores. Using linked credit score data from TransUnion and longitudinal panel survey data from 2023-2025, we aimed to 1) assess the relationship between incident depression and next-year consumer credit scores and 2) identify whether household savings modified the relationship, if any, between incident depression and credit scores. We used data from the Cumulative Life Stressors Impact on Mental Health and Well-Being (CLIMB) Study, a nationally representative survey of US adults collected annually in Spring of 2023, 2024, and 2025 and linked continuous, longitudinal credit scores for consenting adults (n=720). Incident depression was defined as screening positive for depression (PHQ-9≥10) in 2024 after screening negative in 2023. We used linear regression to model next-year credit scores for adults experiencing incident depression, adjusting for sex, race and ethnicity, age, education, household income, household savings, home ownership, Census region, and household size. We then estimated the predicted levels of next-year credit scores within incident depression and household savings groups using a second adjusted linear regression model with an interaction term between incident depression and household savings. In 2024, 64 (8.9%) adults with incident depression. Reporting incident depression was associated with an unadjusted estimated decrease of 63.9 points (95% CI: -92.7, -35.1) in next-year credit score; adjusted models estimated a decrease of 37.2 points (95% CI: -62.2, -12.2) in credit scores. Among adults with incident depression, individuals with savings below $5,000 had a 97.3 point (95% CI: -152.2, -42.3) lower credit score compared to individuals with savings higher than $5,000. In conclusion, incident depression was associated with meaningful drops in next-year credit scores; this association was more pronounced among persons with lower savings.