Substance Use

Alcohol tax policy, alcohol consumption, and depressive symptoms in the Health and Retirement Study Peter Toyokazu Buto* Peter Buto Minhyuk Choi Scott C. Zimmerman Justin S. White Laura Schmidt Stacy Sterling Shelli Vodovozov Yvette Cozier Suzanna M. Martinez Rhoda Au Felicia W. Chi M. Maria Glymour

Evidence suggests a bidirectional relationship between alcohol consumption and depressive symptoms, but the magnitude of effects can be challenging to estimate. We used an instrumental variable (IV) analysis to assess whether tax-induced alterations in alcohol consumption influenced depressive symptoms.

Our sample included those who joined the Health and Retirement Study (HRS) in 1998 or later, and followed them through 2018. We linked state-level alcohol tax rates from the Alcohol Policy Information System to HRS participants based on current state of residence in each year.

Alcohol consumption was measured as the average number of drinks per week in the last three months. Depressive symptoms were assessed using a modified version of the 8-item Centers for Epidemiologic Study-Depression (CES-D). Covariates included age, sex, race/ethnicity, education, and state of residence.

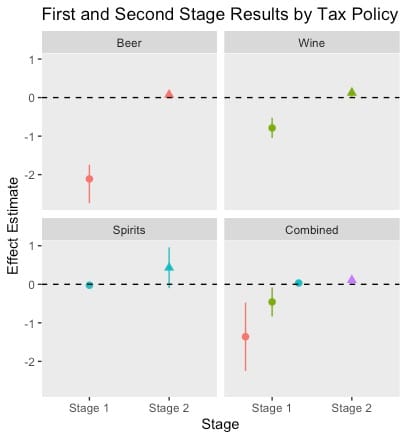

We examined the association of state-level taxes with alcohol consumption. Alcohol tax was modeled separately as the tax on beer, wine, or spirits per gallon and combined. We then conducted two-stage least squares IV for the effect of alcohol use on CES-D.

Our final analytic sample (n=20,774) had an average follow-up of nine years. The average taxes for beer, wine, and spirits over this period across all states were $0.34, $1.22, and $7.29 per gallon, respectively.

For every $1/gallon increase in beer tax, alcohol consumption on average decreased by -2.11 (-2.74, -1.74) drinks/week. Using the combined taxes as an instrument, the IV estimated effect of each additional drink per week was an increase of 0.11 (0.01, 0.20) points of CES-D score. Estimated effects when individually using beer, wine, or spirit taxes as an IV varied slightly but were statistically indistinguishable.

Alcohol taxes were associated with decreased alcohol consumption. These differences, which varied by the type of alcohol tax, were further associated with increased depressive symptoms.